The Market Reporter

Published Weekly by the

United States Department of Agriculture

Bureau of Markets and Crop Estimates

| Washington, D. C. | OCTOBER 8, 1921. | Vol. 4, No. 15 |

The Project Gutenberg EBook of The Market Reporter, by Various

This eBook is for the use of anyone anywhere in the United States and

most other parts of the world at no cost and with almost no restrictions

whatsoever. You may copy it, give it away or re-use it under the terms

of the Project Gutenberg License included with this eBook or online at

www.gutenberg.org. If you are not located in the United States, you'll

have to check the laws of the country where you are located before using

this ebook.

Title: The Market Reporter

Vol. 4, No. 15

Author: Various

Release Date: December 9, 2018 [EBook #58445]

Language: English

Character set encoding: ISO-8859-1

*** START OF THIS PROJECT GUTENBERG EBOOK THE MARKET REPORTER ***

Produced by The Online Distributed Proofreading Team at

http://www.pgdp.net (This file was produced from images

generously made available by The Internet Archive)

Please see the Transcriber’s Notes at the end of this text.

Published Weekly by the

United States Department of Agriculture

Bureau of Markets and Crop Estimates

| Washington, D. C. | OCTOBER 8, 1921. | Vol. 4, No. 15 |

The movement of red clover seed from growers’ hands has been below normal, but that of alsike clover has been fully normal, according to reports received by the Bureau of Markets and Crop Estimates during the week ending Oct. 1. There is a tendency on the part of the growers of red clover seed to hold their seed because the crop, which is now being thrashed in many sections, is not turning out any better than was expected at harvest time and as reported in The Market Reporter for Sept. 10.

Although clover prices on Sept. 27 were mostly 50¢ to $1 per 100 lbs. lower than they were a month ago, they have shown little or no change during the past week or ten days. The quality of red and alsike clover is about equal or slightly inferior to that of last year’s stock. Rains during the last two weeks of September have discolored or bleached much of the seed in some sections.

Red Clover.—In a number of important sections only 5 to 25% of the red clover seed crop had been sold by growers at the end of September. This season’s movement, however, has exceeded the belated movement of the 1920 crop, but has been a little slower than usual. Growers see evidences of a short crop in their immediate vicinity, and in view of the fact that prices offered are on an average $2 to $4 per 100 lbs. lower than last year, and $25 to $28 lower than two years ago at a corresponding time, they are not inclined to sell freely. In a few sections, particularly southwestern Ohio and southeastern Iowa, the movement has been considerably above normal, the growers already having sold 45% and 35%, respectively, of their crops.

The average prices offered to growers in various sections on Sept. 27 for clean seed, as shown in the accompanying table, ranged from $14.60 per 100 lbs. in southwestern Iowa to $17.25 in southwestern Ohio, compared with a range of $17.25 to $22 at a corresponding time last year.

The imports of red clover seed during July, August, and September totaled 1,792,900 lbs. compared with 305,200 lbs. during the same months a year ago. These heavy imports of old seed from Europe and South America have tended to depress prices for domestic seed. French, German, and Italian correspondents state that large quantities of red clover seed were sold during July and August and consequently stocks of old seed have been reduced greatly. The 1921 crop in these and other European countries was reported to be much below normal because of the drought during the summer, and it will be needed for sowing the acreage there next spring.

The quality of the seed in this country varies considerably in different sections, being better than last year in southern Wisconsin, Ohio, Minnesota, South Dakota, and Idaho and somewhat poorer in central Illinois, and Indiana, Michigan, and parts of other States.

Alsike Clover.—In practically all of the important producing sections a larger percentage of the crop had left growers’ hands by Oct. 1 than on the same date last year. It is estimated that about two-fifths of the marketable surplus had been sold by growers by that date. On Sept. 27 growers were being offered $13.05 to $16 per 100 lbs. for clean seed compared with prices a year ago of $18.40 to $24.50 and two years ago of $36.20 to $40.

Most of the reports indicated that the quality of the 1921 crop was approximately the same as that of last year; the reports indicating a difference in quality between the 1921 and 1920 crops were about equally divided, some stating that the quality was better and others stating that it was inferior.

The imports of alsike clover seed from July 1 to Sept. 30 were 1,106,700 lbs., compared with 109,700 lbs. for the same period last year. The crop in Ontario, Canada, which contributes the large bulk of the alsike clover seed that is annually imported into this country is less than normal and is estimated to be 60% of the 1920 crop. The decreased production of this seed in the United States and Canada has caused prices to remain rather firm since harvest.

| Red Clover Seed Prices and Movement. | ||||||

|---|---|---|---|---|---|---|

| State or section. |

Prices offered growers per 100 lbs., basis clean seed. |

Percentage of 1921, 1920, and 1919 crops sold by growers by— |

||||

| Sept. 27, 1921. |

Oct. 5, 1920. |

Sept. 30, 1919. |

Sept. 27, 1921. |

Oct. 5, 1920. |

Sept. 30, 1919. |

|

| P. ct. | P. ct. | P. ct. | ||||

| Michigan | $16.10 | $20.50 | $43.40 | 5 | 5 | 2 |

| N. Illinois | 15.40 | 21.00 | ... | 5 | 10 | 12 |

| C. Illinois | 15.75 | 19.50 | 42.90 | 25 | 15 | 65 |

| N. Indiana | 16.70 | 19.65 | 41.75 | 25 | 15 | 50 |

| C. Indiana | 16.40 | 19.40 | ... | 30 | 10 | 15 |

| S. Indiana | 15.80 | 17.25 | ... | 20 | 10 | 10 |

| NW. Ohio | 15.75 | 20.00 | 44.50 | 45 | 8 | 20 |

| SW. Ohio | 17.25 | 21.75 | ... | 5 | 9 | ... |

| Minnesota | 15.65 | 20.10 | 43.75 | 10 | 3 | 15 |

| W. Wisconsin | 16.05 | 19.80 | ... | 5 | 5 | 10 |

| E. Wisconsin | 17.20 | 20.50 | ... | 5 | 5 | 5 |

| S. Wisconsin | 16.90 | 20.90 | 44.20 | 15 | 6 | 35 |

| Idaho | 15.00 | 22.00 | 43.70 | 10 | 6 | 20 |

| Nebraska | 15.00 | 20.00 | 43.15 | 5 | 4 | 20 |

| Kansas | 14.75 | 17.75 | ... | 15 | 2 | 35 |

| NE. Iowa | 15.50 | 20.00 | ... | 20 | 17 | 5 |

| SW. Iowa | 14.60 | 19.50 | ... | 10 | 5 | 30 |

| SE. Iowa | 15.10 | 21.00 | 41.00 | 35 | 5 | 35 |

| Missouri | 15.90 | 18.75 | ... | 15 | 6 | 50 |

| Alsike Clover Seed Prices and Movement. | ||||||

| P. ct. | P. ct. | P. ct. | ||||

| Michigan | $15.15 | $20.40 | $38.00 | 15 | 6 | 55 |

| N. Illinois | 13.90 | 20.90 | ... | 40 | 11 | 85 |

| C. Illinois | 13.85 | 18.40 | 40.00 | 20 | 20 | 65 |

| N. Indiana | 13.95 | 19.80 | ... | 60 | 36 | 50 |

| C. Indiana | 14.25 | 20.25 | 40.00 | 50 | 14 | 10 |

| NW. Ohio | 13.05 | 21.70 | 38.70 | 60 | 16 | 85 |

| SW. Ohio | 14.45 | 22.90 | ... | 15 | 7 | ... |

| New York | 16.00 | 23.25 | ... | 35 | 5 | 45 |

| W. Wisconsin | 14.00 | 20.30 | ... | 5 | 8 | 45 |

| E. Wisconsin | 14.50 | 21.70 | ... | 15 | 10 | ... |

| S. Wisconsin | 14.60 | 24.50 | 36.20 | 40 | 20 | 35 |

| Idaho | 16.00 | 23.00 | 39.50 | 70 | 10 | 60 |

| Oregon | 14.25 | 22.75 | ... | 60 | 10 | 35 |

Heavy receipts featured the week’s live-stock trading. The trend of cattle prices was decidedly irregular. The hog market had a fairly healthy tone. Sheep and lamb trade showed some improvement. The fresh meat trade throughout the month of September was narrow (pp. 226 and 228).

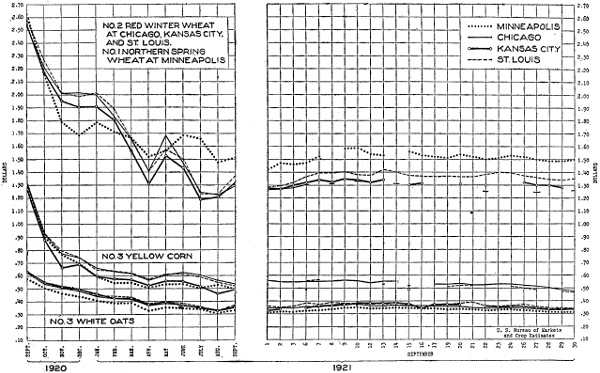

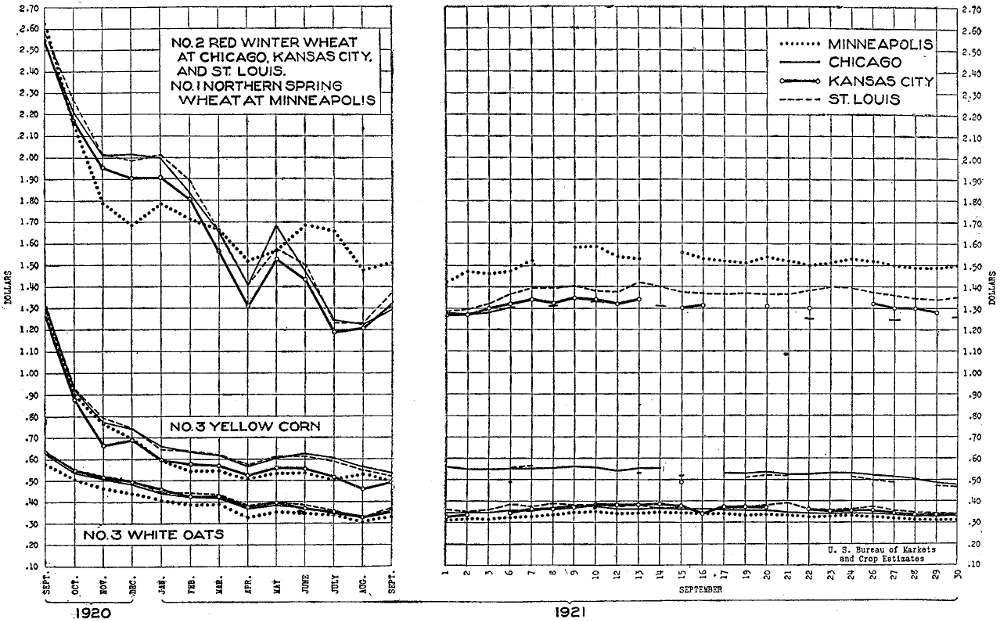

Prices of wheat and corn futures declined steadily throughout the week, but cash premiums strengthened in all markets excepting Minneapolis (p. 234).

The movement of fruits and vegetables was near the peak of the season, and prices declined (p. 230).

Definite information concerning volume of Danish imports steadied the butter market. Cheese markets were steady under improved demand (p. 233).

Hay continued in light supply and prices in most markets were unchanged. General inactivity continued in feed markets, wheat mill feeds registering extreme Weakness (p. 236).

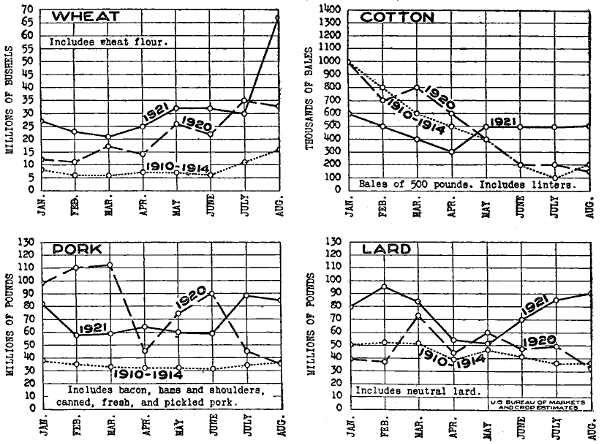

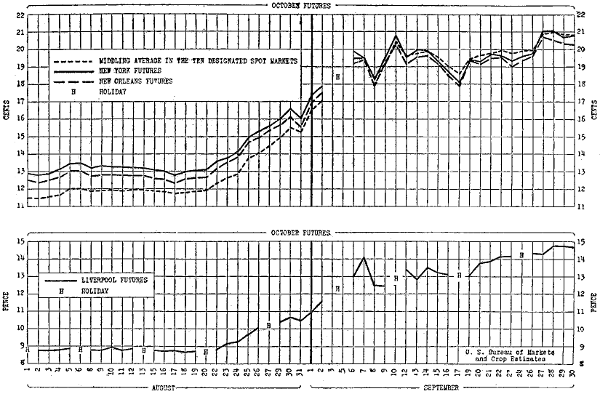

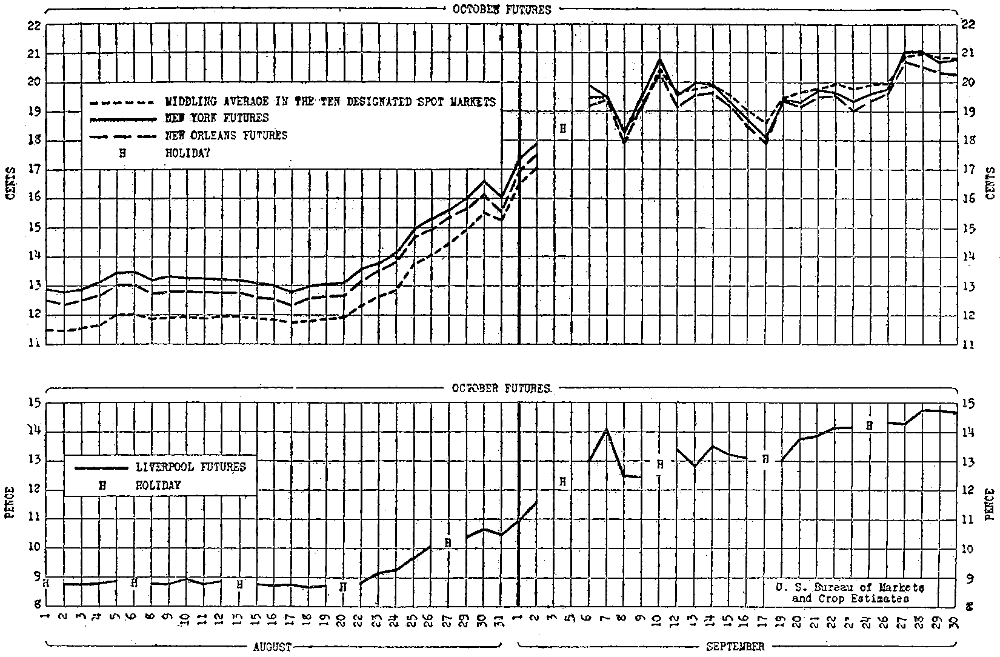

Prices of spot and future cotton continued to advance. Production estimated at only 6,537,000 bales (p. 238).

The monthly Wool consumption report appears on page 239.

The monthly table showing carload shipments of fruits and vegetables appears on page 232.

The movement of unsweetened evaporated milk in cases during August was considerably larger than that of sweetened condensed milk, and the tone of the market for the former class of goods was proportionately better, as shown by a review of the latest available reports from milk manufacturers. The demand for bulk goods has decreased materially with the approach of cooler weather, especially the demand from the ice-cream trade.

Manufacturers’ reports of total stocks on hand Sept. 1 indicate approximately the same surplus of condensed case goods as on Aug. 1, but show a decrease of over 35% in the quantities of evaporated case goods. A similar condition prevailed with regard to unsold stocks, supplies of condensed case goods being practically the same as on Aug. 1, while stocks of unsold evaporated case goods decreased almost 50%. Stocks of case goods of both condensed and unsweetened evaporated milk on Sept. 1 were less than one-half the quantity reported on hand Sept. 1, 1920.

The export movement during August apparently served to give considerable relief to the general situation. Exports totaling 22,803,000 lbs. of evaporated milk more than doubled the July exports. Exports of condensed milk were but 7,557,000 lbs., although this was 2,000,000 lbs., heavier than in July. The United Kingdom received the heaviest shipments, 12,716,000 lbs. of evaporated and 3,232,000 lbs. of condensed going to that country. France and Germany each received approximately 3,000,000 lbs. of evaporated milk.

Exports of condensed milk during the first eight months of 1921 were but 62,000,000 lbs., compared with more than 221,000,000 lbs. during the same period in 1920, while exports of 116,000,000 lbs. of evaporated milk this year are 5,000,000 lbs. heavier than the shipments in 1920.

Manufacturers’ selling prices to the domestic trade during August remained practically the same as during July, but reductions occurred in prices to foreign trade. The largest cuts averaging 34¢ per case were made in export prices of sweetened condensed milk. Unsweetened evaporated milk prices to foreign trade were not so generally reduced, as some manufacturers seem to have advanced export prices slightly, with the result that the average export price was but 4¢ less per case than during the previous month.

Wholesale Prices of Condensed and Evaporated Milk.

(To domestic trade.)

| Geographic section. |

Sweetened condensed case of 14-oz. cans. |

Unsweetened evaporated case of 16-oz. cans. |

||

|---|---|---|---|---|

| Aug. | July. | Aug. | July. | |

| New England | $6.07 | $6.16 | $4.82 | $4.83 |

| Middle Atlantic | 5.95 | 5.89 | 4.88 | 4.79 |

| South Atlantic | 6.47 | 6.47 | 5.02 | 4.97 |

| East North Central | 6.41 | 6.48 | 4.52 | 4.64 |

| West North Central | 6.38 | 6.44 | 4.76 | 4.75 |

| South Central | 6.49 | 6.53 | 4.91 | 5.05 |

| Western (North) | 6.38 | 6.33 | 4.72 | 4.61 |

| Western (South) | 6.53 | 6.37 | 4.78 | 4.67 |

| United States | 6.28 | 6.26 | 4.83 | 4.78 |

Prices to Producers at Condenseries for 3.5% Milk.

(Per 100 lbs.)

| Geographic section. |

By manufacturers of case and bulk goods. |

By manufacturers of bulk goods only. |

||

|---|---|---|---|---|

| Sept. | Aug. | Sept. | Aug. | |

| New England | $1.91 | $1.91 | $3.30 | $3.30 |

| Middle Atlantic | 2.23 | 2.06 | 2.17 | 2.14 |

| South Atlantic | 2.15 | 1.88 | 1.66 | 1.87 |

| East North Central | 1.84 | 1.85 | 1.88 | 1.87 |

| West North Central | 1.80 | 1.80 | 1.77 | 1.40 |

| Western (North) | 1.77 | 1.53 | 2.23 | 2.30 |

| Western (South) | 1.73 | 1.61 | ... | ... |

| United States | 1.87 | 1.87 | 2.04 | 2.06 |

Stocks and Exports of Condensed and Evaporated Milk.

[In thousands of pounds; i. e., 000 omitted.]

| Stocks. | Sept. 1, 1921. |

Aug. 1, 1921. |

Sept. 1, 1920. |

|||

|---|---|---|---|---|---|---|

| Case goods. |

Bulk goods. |

Case goods. |

Bulk goods. |

Case goods. |

Bulk goods. |

|

| CONDENSED. | ||||||

| Total stocks | 31,773 | 26,654 | 30,541 | 28,529 | 71,341 | 32,766 |

| Total unsold stocks | 21,574 | 19,074 | 21,588 | 24,476 | 58,577 | 8,733 |

| Total unfilled orders | 339 | ... | 425 | 14 | 300 | ... |

| EVAPORATED. | ||||||

| Total stocks | 90,503 | 770 | 145,867 | 739 | 170,198 | 851 |

| Total unsold stocks | 36,149 | 763 | 68,658 | 719 | 103,812 | 738 |

| Total unfilled orders | 6,039 | ... | 10,025 | ... | 3,482 | ... |

| Exports. | Aug., 1921. |

July, 1921. |

Aug., 1920. |

|---|---|---|---|

| Condensed milk | 7,557 | 5,727 | 20,503 |

| Evaporated milk | 22,803 | 11,611 | 5,100 |

| Total | 30,360 | 17,338 | 25,603 |

(Chicago, East St. Louis, Kansas City, Omaha, and St. Paul.)

Receipts of live stock during the closing week of September were of generous volume despite the fact that conditions in some departments of the trade during the preceding week bordered on demoralization. An increased proportion of trashy, light-weight cattle indicated that producers were anxious to liquidate surplus holdings before stormy weather sets in, while a corresponding decrease in receipts of corn-feds suggested a decreased number of well-conditioned beef cattle in feeders’ hands.

Chicago’s cattle receipts for the week were the largest since January, while the combined ten-market supply of about 242,300 cattle was practically the same as the week previous but 41,000 short of the corresponding week a year ago.

Following the descent of hog prices during the preceding week to the lowest levels of the year, the marketward movement of hogs expanded materially, the ten-market total at approximately 436,000 being 40,000 in excess of the week previous, and nearly 60,000 greater than the same week last year. The hog run, while continuing to carry an abnormally large proportion of heavy packing sows for this period of the year, showed a considerably enlarged quota Of spring-farrowed, light and underweight stock and average weights decreased at most points. The disposition shown by producers in many sections to unload pigs and immature light hogs was anything but a bullish influence on prices but a revival of eastern shipping demand assisted in checking the decline.

Receipts of sheep and lambs for the week both at Chicago and numerous other western points were the largest of the year, the ten-market total of about 419,500 exceeding the previous week’s supply by approximately 38,000 and being nearly 1,000 in excess of those of the same week last year. The crop, however, carried a heavy proportion of feeders from the western range and the market displayed gratifying stability following the slump in prices during the week previous, which was one of the most severe slumps of the season.

Cattle.—Higher prices for most grades of beef steers showing effective corn feeding, further seasonal expansion in the movement of both native and western grass cattle, and further evidences of increasing interest on the part of stocker and feeder buyers featured the cattle trade during the week under review. The trend of prices at the different market centers was decidedly irregular. Omaha, where receipts were considerably lighter than the preceding week, showed advances on practically all classes of cattle. Other River markets under review showed irregular declines on grass cattle and comparatively little change on desirable corn-feds. At Chicago, where receipts of northwestern range cattle were nearly double the largest previous run this season, grass steers and the less desirable of the warmed-up and plain, heavy, fed steers sold steady to 25¢ lower, and the better grades of corn-fed steers, including yearlings, all the way from 10¢ to 50¢ higher.

The return of $11 cattle after an absence dating back to last January, marked the week’s trading at Chicago. Two lots of prime Angus and Hereford yearlings averaging 985 lbs. and 891 lbs., respectively, brought that price. The former consignment was made up of natives from an Iowa feed lot, nearly half of which were heifers. The other lot consisted of Illinois-fed, branded steers which originally came from Texas.

The popularity at all market centers of well-finished yearlings on the baby beef order and of finished 1,100-lb. to 1,300-lb. steers over the weighty and more aged bullocks was as pronounced as ever, and the price premiums earned by the former were unprecedented for this season of the year. Thick-fat 1,400-lb. to 1,500-lb. steers of high quality and closely approaching prime grade could not pass $9.25 at Chicago and contrasted oddly with the moderately fat, short-fed yearlings that brought about the same figure. Ripe steers in the 1,600-lb. to 1,760-lb. class that had been grain-fed a year or more, sold at Chicago and Omaha at $8.25 to $8.50 with a plainer, weighty kind that had consumed considerable corn, down to $7.50. Many sales of good and choice 1,200-lb. to 1,350-lb. steers between $8 and $8.75 were made at Chicago and elsewhere. A few loads of long yearlings averaging 1,100 lbs. to 1,175 lbs. sold as high as $10 and $10.50.

A generous proportion of the run, however, all around the western market circuit consisted of branded and native grass steers of mediocre and medium killing quality that cashed at $5 to $6.50, comparatively few straight grass steers being good enough to bring $7. This was true despite the fact that two loads of Montanas reached $7.25 at Chicago. Light grass steers of common quality but carrying enough flesh to make cheap carcass beef, sold as low as $4.25 and $4.50 at St. Paul and Missouri River points and a few, chiefly on the Mexican order, ranged downward from $5 at Chicago.

An increase of nearly 50% in receipts of northwestern grass cattle at Chicago was credited in part to the 20% cut in long-haul freight rates. The week’s total of about 13,000 cattle from that source, however, was but little more than half as large as similar receipts during the corresponding week last year. It seems probable, however, that the Northwest will ship more freely during October, as after this month stormy weather is likely to put an end to cattle roundups.

Liberal receipts of low and medium grade steers and their cheapness “on the hooks” as compared with most grades of she stock had a depressing effect on cow and heifer prices at all markets covered by this report except Omaha. At the latter market light receipts forced cow prices up along with those of most other classes of cattle. Canners and choice dry-fed heifer yearlings withstood the downward tendency and held about steady.

The break in she-stock prices ranged anywhere from 25¢. to $1. Declines were most severe at Chicago, where medium to good grades of fat cows and the same classes of grass heifers frequently showed a break of 75¢. to $1 compared with the previous week-end. A spread of $3.75 to $5.75 took the big end of the week’s supply of grass cows and heifers, while canners and cutters ranged largely from $2.25 to $3.25. The best of the light, corn-fed heifer yearlings sold well in line with finished steer yearlings, but they had to be of the baby-beef type. Owing to scarcity of corn-fed cows and a slackened demand for kosher cows due to the approaching Jewish holidays, few heavy cows were good enough to bring $6 at any of the large western markets.

Bulls sold steady to lower at most points, while calves were sharply lower at both Chicago and St. Paul, little changed at Kansas City and St. Louis, and higher at Omaha because of meager receipts.

The demand for stock and feeding cattle, which has been gaining breadth during recent weeks, was comparatively liberal during the closing week of September and the total movement to the country was the largest of the year to date. Except Omaha, where stocker and feeder cattle shared in the general price upturn, prices of such cattle at points under review were at the lowest levels of the year to date. Well-bred yearlings and light feeders were in strongest demand.

With the exception of a few steers on the fat cattle order, few cattle went to the country costing over $6.75. The bulk of the feeder steers sold within a range of $5.25 to $6.25 and stockers largely between $5 and $6. Some of the best stock steers, however, sold right up with the choice heavy feeders and many plain and common light stockers sold downward from $4.50. Kansas City reported a fully steady market for stock cows and heifers with a good many cows going out at $3.50 to $4, and many stock heifers at $4 to $5 with a few as high as $5.50.

RECEIPTS, SHIPMENTS, AND LOCAL SLAUGHTER FOR THE WEEK ENDING OCT. 1.

| Markets. | Cattle and calves. | Hogs. | Sheep. | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Re- ceipts. |

Ship- ments. |

Local slaugh- ter. |

Re- ceipts. |

Ship- ments. |

Local slaugh- ter. |

Re- ceipts. |

Ship- ments. |

Local slaugh- ter. |

|

| Chicago | 79,076 | 25,332 | 53,744 | 126,432 | 27,148 | 99,284 | 148,779 | 57,903 | 90,876 |

| Denver[1] | 9,482 | 7,767 | 2,272 | 2,793 | ... | 2,675 | 44,713 | 34,469 | 4,086 |

| East St. Louis | 30,067 | 14,640 | 10,101 | 48,094 | 17,536 | 22,904 | 7,434 | 1,081 | 4,062 |

| Indianapolis[1] | 9,533 | 4,398 | 4,919 | 60,437 | 32,349 | 27,399 | 2,823 | 1,547 | 1,323 |

| Kansas City | 78,446 | 43,851 | 31,002 | 28,914 | 8,109 | 20,926 | 47,121 | 12,179 | 24,234 |

| Oklahoma City | 7,767 | 2,509 | 4,557 | 4,574 | 272 | 4,142 | 165 | ... | 165 |

| Omaha | 35,557 | 23,657 | 11,900 | 30,607 | 5,687 | 24,920 | 126,966 | 73,496 | 53,470 |

| St. Joseph[1] | 13,639 | 5,006 | 9,101 | 21,122 | 2,953 | 17,541 | 28,565 | 8,123 | 17,545 |

| St. Paul[1] | 24,301 | 13,023 | 12,163 | 31,339 | 4,445 | 27,035 | 19,209 | 6,823 | 12,381 |

| Sioux City | 15,032 | 11,659 | 4,296 | 28,068 | 9,874 | 16,285 | 8,242 | 4,293 | 4,564 |

| Wichita[1] | 7,554 | 5,422 | 2,415 | 4,236 | 127 | 4,270 | 399 | 251 | 169 |

| Total | 310,456 | 157,264 | 146,470 | 356,616 | 108,560 | 267,381 | 434,416 | 260,165 | 222,875 |

| Previous week | 324,438 | 153,997 | 154,269 | 373,574 | 100,615 | 258,235 | 403,963 | 169,947 | 213,446 |

[1] Week ending Friday, Sept. 30.

DAILY AVERAGE WEIGHT AND COST OF HOGS FOR WEEK ENDING OCT. 1.

[Price per 100 lbs.]

| Mon. | Tues. | Wed. | Thurs. | Fri. | Sat. | This wk. | Last wk. | 1 yr. ago. | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Wt. | Cost. | Wt. | Cost. | Wt. | Cost. | Wt. | Cost. | Wt. | Cost. | Wt. | Cost. | Wt. | Cost. | Wt. | Cost. | Wt. | Cost. | |

| Chicago | 272 | $7.10 | 255 | $7.29 | 262 | $7.31 | 246 | $7.30 | 246 | $7.43 | 280 | $7.06 | 259 | $7.25 | 263 | $7.42 | 247 | $15.74 |

| E. St. Louis | 195 | 8.22 | 188 | 8.16 | 188 | 8.16 | 204 | 8.00 | 209 | 7.94 | 201 | 8.10 | 198 | 8.10 | 192 | 8.17 | 196 | 16.35 |

| Kansas City | 209 | 7.53 | 209 | 7.52 | 209 | 7.54 | 225 | 7.35 | 221 | 7.23 | 270 | 7.33 | 213 | 7.46 | 213 | 7.77 | 220 | 15.79 |

| Omaha | 304 | 6.41 | 292 | 6.61 | 289 | 6.84 | 300 | 6.44 | 290 | 6.96 | 292 | 6.41 | 294 | 6.55 | 299 | 6.86 | 273 | 15.72 |

| S. St. Paul | 243 | 6.58 | 235 | 6.83 | 245 | 6.95 | 236 | 6.95 | 246 | 7.20 | 211 | 7.02 | 240 | 6.86 | 236 | 7.16 | ... | ... |

| The above prices are computed on packer and shipper purchases. | ||||||||||||||||||

| Mon. | Tues. | Wed. | Thurs. | Fri. | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Wt. | Cost. | Wt. | Cost. | Wt. | Cost. | Wt. | Cost. | Wt. | Cost. | |

| Chicago | 272 | $7.10 | 255 | $7.29 | 262 | $7.31 | 246 | $7.30 | 246 | $7.43 |

| E. St. Louis | 195 | 8.22 | 188 | 8.16 | 188 | 8.16 | 204 | 8.00 | 209 | 7.94 |

| Kansas City | 209 | 7.53 | 209 | 7.52 | 209 | 7.54 | 225 | 7.35 | 221 | 7.23 |

| Omaha | 304 | 6.41 | 292 | 6.61 | 289 | 6.84 | 300 | 6.44 | 290 | 6.96 |

| S. St. Paul | 243 | 6.58 | 235 | 6.83 | 245 | 6.95 | 236 | 6.95 | 246 | 7.20 |

| Sat. | This wk. | Last wk. | 1 yr. ago. | |||||

|---|---|---|---|---|---|---|---|---|

| Wt. | Cost. | Wt. | Cost. | Wt. | Cost. | Wt. | Cost. | |

| Chicago | 280 | $7.06 | 259 | $7.25 | 263 | $7.42 | 247 | $15.74 |

| E. St. Louis | 201 | 8.10 | 198 | 8.10 | 192 | 8.17 | 196 | 16.35 |

| Kansas City | 270 | 7.33 | 213 | 7.46 | 213 | 7.77 | 220 | 15.79 |

| Omaha | 292 | 6.41 | 294 | 6.55 | 299 | 6.86 | 273 | 15.72 |

| S. St. Paul | 211 | 7.02 | 240 | 6.86 | 236 | 7.16 | ... | ... |

| The above prices are computed on packer and shipper purchases. | ||||||||

Hogs.—The hog market had a fairly healthy tone and the erratic fluctuations which marked the trade for several weeks previous were, for the most part, missing. While during the preceding week, average cost of hogs at the markets under review showed a decrease, Chicago prices dropping to the lowest levels since early in 1916, closing prices of the week under review were generally 10¢ to 15¢ higher than the previous week-end. A broader eastern demand was partly responsible for the advance.

While the proportion of new crop hogs showed a seasonal increase at practically all points, the continued heavy receipts of packing sows caused considerable comment. Traders at Chicago do not recall any recent period when receipts at this time of the year carried so large a percentage of packing sows as do current offerings. Packing sows were of almost uniformly good quality, many of them being almost as smooth as barrows. Several of the smaller packers at Chicago turned from heavy barrows to good and choice sows.

Many of the new-crop hogs showed very little finish and buyers complained that many were “dopey” apparently suffering from the effects of initial rations of new corn. On almost every day butcher hogs averaging 200 lbs. to 240 lbs. sold at top prices at Chicago, while the 160-lb. to 170-lb. kinds closed considerably under top quotations.

The closing top at Chicago was $8.30 with the average cost that day $7.06. The average cost of packing and shipping droves for the week at that point was $7.25, with the average weight at 259 lbs., the lightest since the week ending Aug. 6. The closing top at East St. Louis was $8.35, at Kansas City $7.65, at Omaha $7.75, and at St. Paul $7.60.

Sheep.—Considering supplies, which at leading western markets were the heaviest of the year, sheep and lamb trade during the final week of September showed some improvement. Receipts at Chicago were larger than during any previous week since 1919 and range lambs, carrying the largest proportion of feeders of the season, were greatly in the majority.

In the fat classes, supply and demand were evenly balanced and as the feeder outlet developed considerable breadth, closing prices on all classes were practically steady with the close of the week previous.

Sheep were generally steady at all points except Kansas City, where prices worked 25¢ to 50¢ higher on fat classes. Fat lambs closed lower for the week at Omaha and higher at East St. Louis but were little changed elsewhere. Feeder classes sold steady to somewhat higher at all points. The range movement started early this summer and the early season output of feeders was small.

Opening, Oct. 3.—Beef steers were strong to 25¢ higher at Chicago with desirable corn-feds gaining most. River markets were generally steady to strong on corn-feds and slow to lower on grassers. The week opened with a big run of 35,000 cattle at Kansas City. Chicago’s receipts at 20,000 cattle were well below expectations and the supply of good corn-fed cattle showed a marked decrease. Top yearlings reached $11.15 at Chicago, the highest point reached since early in January and within 10¢ of the top for the year on yearlings.

With receipts moderate, hog prices were generally strong to 15¢ higher. East St. Louis reported a 15¢ to 25¢ advance with top hogs at $8.55. At Chicago the top was $8.45 and at Omaha $8, at Kansas City $7.90 and at St. Paul $7.50.

Fat sheep and lambs opened generally steady to 25¢ higher. Western fat lambs topped at $9 at Chicago, $8.50 at Omaha, and $8.40 at Kansas City. Fat natives reached $8.50 at Chicago. The fat ewe top was $4.75 at Chicago, $4.50 at East St. Louis, and $4.25 at Omaha. Best feeder lambs brought $7.25 at Chicago on a firm market and $7 at Omaha.

LIVE STOCK PRICES, TUESDAY, OCT. 4.

[Per 100 lbs.]

| Chicago. | East St. Louis. |

Kansas City. |

Omaha. | St. Paul. | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| HOGS. | |||||||||||||||||

| Top | $8.55 | $8.65 | $8.10 | $8.10 | $7.75 | ||||||||||||

| Bulk of sales | 6.65 | - | 8.40 | 8.25 | - | 8.65 | 7.25 | - | 8.00 | 6.25 | - | 7.50 | 6.50 | - | 7.75 | ||

| Heavy (250 lbs. up), medium-choice | 7.60 | - | 8.40 | 7.50 | - | 8.55 | 7.15 | - | 8.00 | 6.75 | - | 7.50 | 6.75 | - | 7.50 | ||

| Medium (200-250 lbs.), common-choice | 8.20 | - | 8.50 | 8.40 | - | 8.65 | 7.35 | - | 8.10 | 7.00 | - | 8.00 | 6.85 | - | 7.75 | ||

| Light (150-200 lbs.), common-choice | 7.85 | - | 8.50 | 8.25 | - | 8.65 | 7.00 | - | 8.10 | 7.35 | - | 8.10 | 7.35 | - | 7.75 | ||

| Light lights (130-150 lbs.), common-choice | 7.65 | - | 8.20 | 8.15 | - | 8.50 | 6.75 | - | 7.85 | ... | ... | ||||||

| Packing sows (250 lbs. up), smooth | 6.65 | - | 7.25 | 6.25 | - | 6.75 | 6.25 | - | 7.00 | 6.15 | - | 6.65 | 6.25 | - | 6.85 | ||

| Packing sows (250 lbs. up), rough | 6.25 | - | 6.65 | 5.75 | - | 6.25 | 5.50 | - | 6.25 | 5.75 | - | 6.15 | 6.00 | - | 6.40 | ||

| Pigs (150 lbs. down), common-choice | 7.10 | - | 7.75 | 7.65 | - | 8.30 | ... | ... | ... | ||||||||

| Stock pigs (130 lbs. down) | ... | 6.75 | - | 8.25 | 6.50 | - | 8.35 | 7.00 | - | 8.00 | 7.50 | - | 8.25 | ||||

| CATTLE. | |||||||||||||||||

| Beef steers: | |||||||||||||||||

| Medium and heavy (1,100 lbs. up)— | |||||||||||||||||

| Choice and prime | 8.85 | - | 10.90 | 8.75 | - | 10.00 | 8.50 | - | 10.00 | 8.50 | - | 9.75 | ... | ||||

| Good | 8.25 | - | 9.65 | 8.25 | - | 9.25 | 7.00 | - | 9.00 | 7.75 | - | 8.50 | 7.75 | - | 8.75 | ||

| Medium | 6.00 | - | 8.75 | 5.25 | - | 8.25 | 5.25 | - | 7.25 | 5.50 | - | 7.75 | 6.00 | - | 7.75 | ||

| Common | 5.00 | - | 6.00 | 4.50 | - | 5.25 | 4.35 | - | 5.25 | 4.25 | - | 5.50 | 4.25 | - | 5.75 | ||

| Light weight (1,100 lbs. down)— | |||||||||||||||||

| Choice and prime | 10.25 | - | 11.25 | 9.75 | - | 11.00 | 9.50 | - | 10.35 | 9.75 | - | 10.75 | ... | ||||

| Good | 9.00 | - | 10.25 | 8.50 | - | 9.75 | 7.10 | - | 9.50 | 7.50 | - | 9.75 | 8.50 | - | 9.50 | ||

| Medium | 6.00 | - | 9.00 | 4.75 | - | 8.50 | 5.00 | - | 7.40 | 5.25 | - | 7.50 | 6.00 | - | 8.50 | ||

| Common | 4.75 | - | 6.00 | 4.00 | - | 4.75 | 4.00 | - | 5.00 | 4.00 | - | 5.25 | 4.00 | - | 6.00 | ||

| Butcher cattle: | |||||||||||||||||

| Heifers, common-choice | 4.25 | - | 9.25 | 4.25 | - | 10.50 | 3.75 | - | 8.00 | 4.00 | - | 8.75 | 3.50 | - | 8.75 | ||

| Cows, common-choice | 3.50 | - | 6.75 | 3.25 | - | 6.00 | 3.35 | - | 5.50 | 3.75 | - | 6.50 | 3.00 | - | 6.50 | ||

| Bulls, bologna, and beef | 3.65 | - | 6.35 | 3.25 | - | 6.25 | 3.00 | - | 5.25 | 3.00 | - | 6.25 | 2.75 | - | 5.50 | ||

| Canners and cutters: | |||||||||||||||||

| Cows and heifers | 2.50 | - | 3.50 | 2.25 | - | 3.50 | 2.00 | - | 3.35 | 2.25 | - | 3.75 | 1.75 | - | 3.00 | ||

| Canner steers | 3.00 | - | 3.50 | 2.50 | - | 3.00 | 2.50 | - | 3.25 | 2.50 | - | 3.75 | 2.25 | - | 3.00 | ||

| Veal calves: | |||||||||||||||||

| Light and medium weight, medium-choice | 5.50 | - | 11.50 | 6.00 | - | 11.50 | 7.00 | - | 10.00 | 7.00 | - | 10.00 | 5.00 | - | 9.50 | ||

| Heavy weight, common-choice | 3.50 | - | 7.00 | 3.00 | - | 7.00 | 3.00 | - | 6.50 | 3.50 | - | 7.25 | 3.00 | - | 6.00 | ||

| Feeder steers: | |||||||||||||||||

| 1,000 lbs. up, common-choice | 5.00 | - | 6.75 | 5.00 | - | 6.50 | 4.60 | - | 7.00 | 5.00 | - | 7.25 | 3.75 | - | 6.25 | ||

| 750-1,000 lbs., common-choice | 4.85 | - | 6.50 | 4.50 | - | 6.50 | 4.50 | - | 6.90 | 4.75 | - | 7.00 | 3.50 | - | 6.00 | ||

| Stocker cattle: | |||||||||||||||||

| Steers, common-choice | 3.75 | - | 6.50 | 3.50 | - | 6.50 | 3.40 | - | 6.65 | 3.75 | - | 7.00 | 3.25 | - | 6.00 | ||

| Cows and heifers, common-choice | 3.25 | - | 4.75 | 2.50 | - | 5.50 | 2.50 | - | 5.50 | 2.75 | - | 5.50 | 2.50 | - | 4.00 | ||

| Calves: | |||||||||||||||||

| Good and choice | ... | 5.25 | - | 6.25 | 5.50 | - | 6.50 | 5.75 | - | 7.25 | ... | ||||||

| Common and medium | ... | 4.00 | - | 5.00 | 3.25 | - | 5.25 | 3.75 | - | 5.75 | ... | ||||||

| SHEEP. | |||||||||||||||||

| Lambs: | |||||||||||||||||

| 84 lbs. down, medium-choice | 7.25 | - | 9.25 | 6.75 | - | 8.75 | 7.25 | - | 8.75 | 7.25 | - | 8.75 | 6.25 | - | 8.00 | ||

| Culls and common | 4.75 | - | 7.25 | 4.00 | - | 6.50 | 4.00 | - | 7.00 | 4.75 | - | 7.00 | 3.00 | - | 6.00 | ||

| Feeding lambs | 6.00 | - | 7.25 | ... | 5.25 | - | 7.00 | 6.00 | - | 7.25 | 4.50 | - | 6.50 | ||||

| Yearlings, wethers, medium-prime | 5.00 | - | 7.00 | 4.50 | - | 6.00 | 4.50 | - | 6.25 | 5.00 | - | 6.25 | 4.50 | - | 6.25 | ||

| Wethers, medium-prime | 4.00 | - | 5.50 | 3.50 | - | 5.00 | 4.00 | - | 5.25 | 4.00 | - | 5.00 | 3.25 | - | 4.75 | ||

| Ewes: | |||||||||||||||||

| Medium-good and choice | 3.00 | - | 5.00 | 3.00 | - | 4.00 | 3.25 | - | 4.60 | 3.25 | - | 4.50 | 2.75 | - | 4.00 | ||

| Culls and common | 1.50 | - | 2.75 | 1.00 | - | 2.75 | 1.00 | - | 3.00 | 1.50 | - | 3.00 | 1.00 | - | 2.75 | ||

| Breeding ewes (full mouths to yearlings) | 3.25 | - | 6.25 | ... | 3.50 | - | 5.75 | 3.50 | - | 5.25 | ... | ||||||

| Feeding ewes | ... | ... | ... | 2.75 | - | 3.50 | ... | ||||||||||

WHOLESALE PRICES OF WESTERN DRESSED MEATS, TUESDAY, OCT. 4.

[Per 100 lbs.]

| Chicago. | New York. | |||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Oct. 4. | Sept. 27. | Sept. 6. | Oct. 4. | Sept. 27. | Sept. 6. | |||||||||||||||

| Fresh beef: | ||||||||||||||||||||

| Steers— | ||||||||||||||||||||

| Choice | $16.50 | - | 17.50 | $16.50 | - | 17.00 | $17.00 | - | 17.50 | $17.00 | - | 19.00 | $17.00 | - | 19.00 | $18.00 | - | 19.00 | ||

| Good | 15.50 | - | 16.50 | 15.50 | - | 16.50 | 15.50 | - | 16.50 | 14.00 | - | 16.00 | 14.00 | - | 16.00 | 15.00 | - | 17.00 | ||

| Medium | 12.00 | - | 14.00 | 12.00 | - | 14.00 | 11.50 | - | 14.00 | 11.00 | - | 13.00 | 12.00 | - | 13.50 | 13.00 | - | 14.00 | ||

| Common | 8.50 | - | 10.00 | 8.50 | - | 10.00 | 8.50 | - | 10.50 | 9.00 | - | 10.00 | 10.00 | - | 11.00 | 9.00 | - | 12.00 | ||

| Cows— | ||||||||||||||||||||

| Good | 11.50 | - | 12.00 | 11.50 | - | 12.00 | 11.00 | - | 11.50 | ... | 10.00 | - | 11.00 | 11.00 | - | 12.00 | ||||

| Medium | 10.00 | - | 11.00 | 10.00 | - | 11.00 | 9.50 | - | 10.50 | 9.00 | - | 10.00 | 9.00 | - | 10.00 | 9.00 | - | 10.00 | ||

| Common | 8.00 | - | 9.00 | 7.50 | - | 9.00 | 8.00 | - | 9.00 | 8.00 | - | 9.00 | 8.00 | - | 9.00 | 8.00 | - | 9.00 | ||

| Bulls— | ||||||||||||||||||||

| Common | 7.75 | - | 8.25 | 7.75 | - | 8.25 | 7.50 | - | 8.00 | 8.00 | - | 9.00 | 8.50 | - | 9.00 | 7.00 | - | 7.50 | ||

| Fresh lamb and mutton: | ||||||||||||||||||||

| Lamb— | ||||||||||||||||||||

| Choice | 17.00 | - | 18.00 | 18.00 | - | 19.00 | 19.00 | - | 20.00 | 18.00 | - | 19.00 | 19.00 | - | 20.00 | 20.00 | - | 21.00 | ||

| Good | 15.00 | - | 16.00 | 16.00 | - | 17.00 | 17.00 | - | 18.00 | 16.00 | - | 17.00 | 16.00 | - | 18.00 | 19.00 | - | 20.00 | ||

| Medium | 13.00 | - | 14.00 | 14.00 | - | 15.00 | 15.00 | - | 16.00 | 15.00 | - | 16.00 | 15.00 | - | 16.00 | 16.00 | - | 18.00 | ||

| Common | 10.00 | - | 12.00 | 10.00 | - | 12.00 | 12.00 | - | 14.00 | 10.00 | - | 14.00 | 10.00 | - | 14.00 | 10.00 | - | 15.00 | ||

| Mutton— | ||||||||||||||||||||

| Good | 9.00 | - | 10.00 | 9.00 | - | 10.00 | 10.50 | - | 11.00 | 11.00 | - | 12.00 | 12.00 | - | 13.00 | 11.00 | - | 13.00 | ||

| Medium | 7.00 | - | 8.00 | 7.00 | - | 8.00 | 9.00 | - | 10.00 | 10.00 | - | 11.00 | 10.00 | - | 11.00 | 10.00 | - | 11.00 | ||

| Common | 6.00 | - | 7.00 | 6.00 | - | 7.00 | 6.00 | - | 8.00 | 7.00 | - | 9.00 | 7.00 | - | 9.00 | 5.00 | - | 9.00 | ||

| Fresh veal: | ||||||||||||||||||||

| Choice | 19.00 | - | 20.00 | 19.00 | - | 21.00 | 20.00 | - | 22.00 | 21.00 | - | 22.00 | 23.00 | - | 25.00 | 25.00 | - | 26.00 | ||

| Good | 16.00 | - | 18.00 | 17.00 | - | 19.00 | 19.00 | - | 20.00 | 18.00 | - | 20.00 | 19.00 | - | 21.00 | 22.00 | - | 24.00 | ||

| Medium | 13.00 | - | 15.00 | 12.00 | - | 14.00 | 16.00 | - | 18.00 | 14.00 | - | 17.00 | 15.00 | - | 18.00 | 19.00 | - | 20.00 | ||

| Common | 9.00 | - | 12.00 | 8.00 | - | 11.00 | 12.00 | - | 15.00 | 8.00 | - | 10.00 | 9.00 | - | 12.00 | 14.00 | - | 17.00 | ||

| Fresh pork cuts: | ||||||||||||||||||||

| Loins— | ||||||||||||||||||||

| 8-10 lbs. average | 24.00 | - | 26.00 | 25.00 | - | 27.00 | 29.00 | - | 30.00 | 27.00 | - | 28.00 | 23.00 | - | 30.00 | 29.00 | - | 30.00 | ||

| 10-12 lbs. average | 20.00 | - | 22.00 | 21.00 | - | 23.00 | 27.00 | - | 28.00 | 25.00 | - | 26.00 | 27.00 | - | 20.00 | 26.00 | - | 28.00 | ||

| 12-14 lbs. average | 18.00 | - | 20.00 | 18.00 | - | 20.00 | 22.00 | - | 25.00 | 21.00 | - | 23.00 | 24.00 | - | 25.00 | 23.00 | - | 25.00 | ||

| 14-16 lbs. average | 16.00 | - | 18.00 | 16.00 | - | 18.00 | 19.00 | - | 21.00 | 18.00 | - | 20.00 | 18.00 | - | 20.00 | 20.00 | - | 21.00 | ||

| 16 lbs. and over | 12.00 | - | 15.00 | 13.00 | - | 15.00 | 15.00 | - | 18.00 | 15.00 | - | 18.00 | 16.00 | - | 18.00 | 17.00 | - | 18.00 | ||

| Shoulders— | ||||||||||||||||||||

| Skinned | 13.00 | - | 14.00 | 14.00 | - | 15.00 | 14.50 | - | 15.00 | 14.00 | - | 15.00 | 15.00 | - | 16.00 | 15.00 | - | 16.00 | ||

| Picnics— | ||||||||||||||||||||

| 4-6 lbs. average | 10.50 | - | 11.00 | 11.00 | - | 11.50 | 12.00 | - | 12.50 | ... | ... | ... | ||||||||

| 6-8 lbs. average | 10.00 | - | 10.50 | 10.00 | - | 11.00 | 11.00 | - | 12.00 | 11.00 | - | 12.00 | 11.00 | - | 12.00 | 13.00 | - | 14.00 | ||

| Butts— | ||||||||||||||||||||

| Boston style | 16.00 | - | 17.00 | 16.00 | - | 17.00 | 18.00 | - | 20.00 | 18.00 | - | 19.00 | 18.00 | - | 20.00 | 17.00 | - | 18.00 | ||

Fresh-meat trade during September was narrow and movements into consumptive channels were considerably less than during August, except for a short period at the beginning of the month when there was a fairly good demand for all classes. Although receipts of some classes were less than normal, week-end accumulations in wholesale markets were frequent and as a rule sharp declines followed.

Supplies of beef at eastern markets were approximately 8,250,000 lbs., or 13,800 carcasses less than a year ago. Veal supplies decreased 6,300 carcasses and mutton 32,000 carcasses. Lamb increased 63,000 carcasses, or 2,500,000 lbs. At eastern points the decrease in supplies of fresh pork from locally slaughtered hogs was more than offset by increased shipments from middle western packing centers and a net increase of 110,000 lbs. for the month was shown.

Beef.—Improved trade conditions which were expected to follow cooler weather did not materialize. Average weekly supplies were less than for several months past, but the demand was curtailed to an even greater extent. With liberal quantities of low-grade beef offered at packing centers, increased supplies of sausage material were available, and prices in most cases were fully 50% below those prevailing a year ago. Comparatively little choice beef was offered at any of the markets, and when it appeared in the form of heavy carcasses it was hard to move, selling only at a heavy discount. Carcasses weighing from 450 to 600 lbs. were the kind most in demand.

With supplies at eastern markets consisting chiefly of medium to good grass-fed steers, prices were uneven and during most of the month tended downward. Boston was relatively steadier than other eastern markets and closed only about $1 lower, while New York and Philadelphia registered sharp weekly fluctuations and closed unevenly $1 to $2 net lower. Although the demand at Chicago was again narrow and showed no apparent improvement over that of the preceding month, price changes were slight. To some extent this was caused by local conditions and the ability to adjust supplies to the demand.

Cow beef constituted a relatively small proportion of the offerings at all markets, and was materially less in quantity than at the same time a year ago. Markets were not generally supplied with bulls, and in most cases daily receipts were insufficient to justify quotations.

While kosher beef markets registered slight weekly fluctuations, the range of prices generally was steady, though somewhat higher than in August. The better grades were in best demand. Because of the near approach of Yom Kippur and other Jewish holidays, kosher killing was discontinued during the closing days of September and any surplus supplies were offered for sale to the regular trade.

Veal.—Liberal offerings of heavy veal carcasses, most of which were of undesirable quality, had a depressing effect on prices in general. Milk-fed veal was scarce, but when available found ready sale at firm prices. Receipts at eastern markets were 6,300 carcasses less than during the corresponding month a year ago, but were more than the trade required. Price ranges were materially widened, with the trend upward during the first week, but sharply downward through the remainder of the month. All markets were similarly affected. Closing prices at eastern markets were unevenly $2 to $3 lower than the opening, with common and medium grades registering the greatest decline. Choice veal at Chicago closed steady to $1 higher, with other grades mostly $2 lower than the opening.

Lamb.—With continued heavy receipts of lambs at live-stock centers, the dressed trade was in a chaotic condition. Although estimated receipts of lamb at seven of the principal live-stock markets showed a decrease of 12% as compared with the same month one year ago, liberal offerings of Canadian lambs at eastern markets more than offset the decrease and intensified the already existing unsettled condition. This, together with the continued unequal demand, assisted in pushing prices of the dressed product below the low point reached in February of the present year. Total supplies at eastern markets exceeded those of the same period a year ago by 2,500,000 lbs., and fluctuations on the different grades amounted to $6.

While Chicago registered smaller fluctuations the trend was steadily downward and closing prices were $2 to $3 below the opening. Although closing prices at eastern markets were slightly above the low spot for the month, trade conditions at the close were generally unsatisfactory to the selling side. At the beginning of the month cold storage holdings were 820,519 lbs. less than a month earlier, but were still considerably above the season’s average during prewar years.

Mutton.—Receipts of mutton at eastern markets decreased 32,000 carcasses as compared with the same period a year ago. This reduction, together with a general improvement in quality over that of the previous month, was the principal factor contributing to a generally steady market in the East, particularly during the last half of the month. With supplies at Chicago consisting largely of heavy bucks and ewes and practically no handyweight wethers, that market declined sharply and closed $1.50 to $2 below the opening.

Pork.—Conditions in the fresh-pork trade were generally unsettled. Sharp weekly fluctuations caused by erratic advances on Mondays, which could not be maintained through the week, were an outstanding feature of the month’s trade at some markets. Supplies of loins at eastern markets were practically the same as a year ago and consisted mostly of frozen or chilled stock, for which there was an uneven demand. The latter sold at a wide range of prices and unevenly $4 to $10 below corresponding averages of fresh loins. Closing prices at eastern markets were only slightly changed from the opening, some averages being 50¢ to $1 lower.

Conditions at Chicago, which has been the high market during the past two months, were materially changed and declines equaling the advances of late July were registered during the last half of September. From the high point of $32 on light average loins, prices had dropped to $26 at the close. Heavier average loins registered similar declines. Shoulder cuts were relatively more stable but were mostly $1 to $1.50 off at the close.

Cured pork and lard.—The domestic demand for cured pork cuts and lard, while fair for the season, was not of sufficient volume to offset the decline in live-stock markets and prices registered sharp declines. Dry salt meats and lard were in relatively better demand than hams, bacon, and picnics, and showed proportionately smaller declines. At the close wholesale prices of hams at Chicago were off $3 to $3.50, bacon $2 to $2.50, and picnics $1.50 to $2. The net decline on lard amounted to 75¢, dry salt backs 50¢ to 75¢, and dry salt bellies about $1. Reacting from the general upward trend of prices during August, compound lard markets were weak and closing prices were unevenly 75¢ to $1.50 under the opening.

STOCKER AND FEEDER SHIPMENTS.

Week ending Friday, Sept. 30.

| Cattle and calves. |

Hogs. | Sheep. | |

|---|---|---|---|

| Market origin: | |||

| Chicago | 11,838 | ... | 41,892 |

| East St. Louis | 6,799 | 551 | 1,289 |

| Fort Worth | 3,097 | 353 | 177 |

| Indianapolis | 1,675 | 537 | 262 |

| Kansas City | 26,728 | 2,428 | 10,674 |

| Oklahoma City | 2,504 | 272 | ... |

| Omaha | 21,578 | ... | 54,992 |

| St. Joseph | 3,611 | 145 | 8,148 |

| St. Paul | 9,745 | 204 | 3,837 |

| Sioux City | 11,497 | 2,223 | 5,651 |

| Wichita | 2,605 | 127 | ... |

| Total | 101,677 | 6,840 | 126,922 |

| Previous week | 93,564 | 5,770 | 80,524 |

| Same week last year | 109,142 | 8,795 | 168,815 |

| State destination: | |||

| Arkansas | 30 | 146 | ... |

| California | 364 | ... | ... |

| Georgia | 78 | ... | ... |

| Idaho | 2 | ... | ... |

| Illinois | 16,394 | 1,016 | 18,285 |

| Indiana | 5,966 | 537 | 13,297 |

| Iowa | 21,252 | 2,564 | 27,640 |

| Kansas | 6,823 | 538 | 1,482 |

| Kentucky | 715 | ... | 1,671 |

| Maryland | 162 | ... | 656 |

| Massachusetts | 24 | ... | ... |

| Michigan | 1,160 | ... | 9,696 |

| Minnesota | 1,899 | 642 | 3,931 |

| Missouri | 13,765 | 431 | 15,310 |

| Nebraska | 17,666 | 563 | 24,891 |

| New Jersey | 19 | ... | ... |

| New York | ... | ... | 884 |

| Ohio | 4,112 | 216 | 4,607 |

| Oklahoma | 3,571 | 126 | ... |

| Pennsylvania | 4,490 | ... | ... |

| South Dakota | 1,201 | ... | 1,877 |

| Tennessee | 26 | ... | ... |

| Texas | 1,190 | 61 | 177 |

| Virginia | 25 | ... | ... |

| West Virginia | 56 | ... | ... |

| Wisconsin | 687 | 1,866 | 2,518 |

| Total | 101,677 | 6,840 | 126,922 |

Iowa led all other States in the number of telephones on farms reported to the Census Bureau on Jan. 1. A total of 2,508,002 farms or 38.9% of all farms in the country, had telephones.

A list containing the names and addresses of 10,000 live-stock raisers and breeders has just been received from the Minister of Agriculture of Brazil. The list also gives the number of animals owned by each producer. The total number of animals represented is 5,227,113.

Of the 10,000 breeders, 1,092 have 1,000 to 5,000 animals; 107 have between 5,000 and 10,000; and 39 have more than 10,000. Three of this latter group have 34,000 animals and one has 85,000. This list has been classified according to the number of animals owned, made up in mimeographed form, and will be sent to interested parties upon request. The list does not show the breed or kind of live stock grown.

Similar lists of breeders in Uruguay, Argentina, Colombia, and Mexico are also available. The list of Uruguayan breeders includes only those who have pure-bred animals and does not give the number owned. They are classified according to the breed raised. The list of Argentine breeders consists of the exhibitors at the Palermo show.

The exports of frozen beef from Argentina during the first seven months of 1921 show a decrease of 3,154,275 quarters, compared with the exports during the corresponding months of 1920, according to statistics compiled by the Review of the River Plate. The exports of chilled beef during the same period increased 601,096 quarters; exports of frozen mutton and lamb increased 1,011,754 and 355,593 carcasses, respectively.

The United Kingdom furnished the chief market for all of the frozen and chilled meats exported from Argentina during the seven months’ period, taking 1,582,035 quarters of frozen beef, 772,162 quarters of chilled beef, 1,468,466 carcasses of frozen mutton, and 586,123 carcasses of frozen lamb.

The following table shows the exports of frozen and chilled beef and frozen mutton and lamb from Argentina for the first seven months of 1921 as compared with the same period in the five preceding years:

| First 7 months of— |

Frozen beef. |

Chilled beef. |

Frozen mutton. |

Frozen lamb. |

|---|---|---|---|---|

| Quarters. | Quarters. | Car- casses. |

Car- casses. |

|

| 1916 | 2,465,408 | 450,628 | 933,964 | 393,116 |

| 1917 | 2,935,365 | 373,083 | 664,540 | 314,435 |

| 1918 | 3,249,649 | 23,544 | 546,161 | 120,012 |

| 1919 | 2,851,533 | 74,598 | 826,958 | 131,826 |

| 1920 | 5,344,635 | 183,114 | 594,727 | 260,943 |

| 1921 | 2,189,360 | 784,210 | 1,606,481 | 616,536 |

CHICAGO WHOLESALE PRICES OF CURED

PORK AND PORK PRODUCTS.

[Per 100 lbs.]

| Sept. 30. | Sept. 23. | Sept. 2. | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Hams, smoked, 14-16 average | $23.50 | - | 24.00 | $24.00 | - | 25.50 | $27.00 | - | 29.00 |

| Hams, fancy 14-16 average | 26.00 | - | 26.75 | 26.00 | - | 28.00 | 30.00 | - | 31.50 |

| Picnics, smoked, 4-8 average | 12.50 | - | 15.00 | 12.50 | - | 14.50 | 14.50 | - | 16.00 |

| Bacon, breakfast, 6-8 average | 23.50 | - | 24.50 | 24.00 | - | 24.50 | 25.00 | - | 27.00 |

| Bacon, fancy, 6-8 average | 34.00 | - | 35.00 | 33.00 | - | 35.50 | 34.00 | - | 38.00 |

| Bellies, D. S., 14-16 average | 14.75 | - | 10.00 | 13.75 | - | 15.75 | 15.00 | - | 15.50 |

| Backs, D. S., 14-16 average | 11.75 | - | 12.25 | 10.25 | - | 11.75 | 11.00 | - | 11.50 |

| Pure lard, tierces | 11.50 | - | 13.75 | 13.00 | - | 13.75 | 13.00 | - | 14.50 |

| Compound lard, tierces | 12.00 | - | 13.00 | 12.25 | - | 12.75 | 11.00 | - | 12.00 |

COLD STORAGE HOLDINGS OF FISH, SEPT. 15.

[Thousands of pounds, i. e., 000 omitted.]

| Varieties. | Sept. 15, 1921. |

Sept. 15, 1920. |

Aug. 15, 1921. |

Aug. 15, 1920. |

Frozen since Aug. 15, 1921. |

|---|---|---|---|---|---|

| FROZEN FISH. | |||||

| Bluefish | 442 | 256 | 282 | 211 | 180 |

| Butterfish | 422 | 615 | 255 | 489 | 203 |

| Ciscoes | 5,841 | 4,999 | 4,444 | 2,152 | 1,875 |

| Cod, bake, pollack | 1,865 | 2,578 | 1,878 | 2,113 | 95 |

| Croakers | 345 | 709 | 331 | 281 | 93 |

| Halibut | 9,125 | 10,340 | 7,693 | 8,630 | 1,363 |

| Herring | 3,870 | 5,405 | 3,715 | 5,480 | 632 |

| Lake trout | 1,043 | 555 | 991 | 554 | 93 |

| Mackerel | 1,603 | 2,678 | 1,696 | 3,015 | 105 |

| Rock fishes | 69 | 200 | 69 | 185 | 4 |

| Sablefish | 978 | 834 | 600 | 597 | 339 |

| Salmon, fall | 836 | 891 | 759 | 815 | 65 |

| Salmon, silver | 1,064 | 540 | 631 | 414 | 453 |

| Salmon,other | 5,262 | 3,248 | 3,419 | 2,281 | 1,664 |

| Sea bass | 61 | 109 | 68 | 122 | 4 |

| Shad | 349 | 502 | 325 | 474 | 28 |

| Shad roe | 43 | 43 | 45 | 49 | ... |

| Smelts, eulachon, etc. | 335 | 116 | 272 | 101 | 65 |

| Squid | 3,017 | 2,163 | 3,177 | 910 | 53 |

| Weakfish | 1,755 | 493 | 1,640 | 449 | 190 |

| Whitefish | 1,782 | 1,016 | 1,587 | 624 | 207 |

| Whiting | 5,258 | 9,649 | 4,974 | 8,630 | 464 |

| Miscellaneous | 9,226 | 8,453 | 8,580 | 8,565 | 1,181 |

| Total | 54,591 | 56,297 | 47,431 | 47,141 | 9,356 |

| CURED FISH. | |||||

| Herring | 16,207 | 22,752 | 11,913 | 22,111 | ... |

| Mild cured salmon | 6,855 | 8,275 | 6,165 | 8,149 | ... |

“It has been announced in the press that Quebec farmers are receiving a few dollars only for grass-fed calves, and from $10 up for cows, steers, etc.,” reports the American vice consul at Montreal. “The farmer sells his steer to the drover for 5¢ a lb. on the hoof. The latter sells to the abattoir for 6¢, and, after he has paid his overhead expenses, freight, shrinkage, etc., he makes an average of about $5 on each animal. The abattoir figures on a profit of about $6 on an average steer. There is little or no profit made on the forequarters, and for this the hind-quarters must compensate.”

ANIMALS SLAUGHTERED UNDER FEDERAL INSPECTION DURING AUGUST.

| Station. | Cattle. | Calves. | Sheep. | Goats. | Swine. |

|---|---|---|---|---|---|

| Chicago | 138,496 | 34,538 | 293,516 | ... | 433,823 |

| Fort Worth | 33,713 | 40,516 | 13,549 | 39 | 27,079 |

| Kansas City | 98,897 | 26,647 | 104,831 | 36 | 167,034 |

| National Stock Yards | 24,516 | 11,105 | 48,312 | 16 | 72,874 |

| Omaha | 61,634 | 4,573 | 184,687 | ... | 123,089 |

| St. Louis | 16,788 | 4,965 | 10,663 | ... | 104,840 |

| Sioux City | 16,637 | 1,137 | 10,883 | ... | 72,845 |

| South St. Joseph | 23,797 | 5,962 | 58,814 | 13 | 105,624 |

| South St. Paul | 19,426 | 21,513 | 33,177 | ... | 96,357 |

| All other establishments | 246,515 | 152,840 | 478,560 | 97 | 1,326,894 |

| Total: | |||||

| August, 1921 | 680,419 | 303,796 | 1,236,992 | 201 | 2,530,459 |

| August, 1920 | 685,763 | 332,349 | 1,041,580 | 1,750 | 2,190,821 |

| 8 months ending August, 1921 | 4,907,174 | 2,526,022 | 8,540,072 | 3,240 | 26,440,048 |

| 8 months ending August, 1920 | 5,413,781 | 2,835,457 | 6,862,931 | 28,826 | 26,239,384 |

Horses slaughtered at all establishments, 175; Inspections of lard prepared at all establishments, 126,026,473 lbs.; compound and other substitutes, 29,823,542 lbs. Corresponding inspections for August, 1920: Lard, 96,527,453 lbs.; compound and other substitutes, 28,322,618 lbs.

Potato prices declined during the week ending Oct. 3 under the heaviest movement of the season. Prices of cabbage and sweet potatoes were lower. Apple prices showed a weaker tone. Other lines were fairly steady. Total shipments of leading lines for the week were 24,033 cars, or about one-third more than during the preceding week. During the corresponding week last year 17,283 cars were moved. The heaviest week’s movement last season was during Oct. 12 to 18, with 27,171 cars.

Potatoes.—Potato shipments reached 10,001 cars during the week ending Oct. 1, thereby increasing the season’s total shipments to 80,560 cars as compared with 65,833 cars moved last year to the same date. The week’s shipments nearly doubled those of last week which were 5,824 cars. Minnesota, the heaviest contributing State, shipped 2,573 cars, North Dakota 1,656 cars, and Maine 1,010 cars. Markets were heavily supplied, demand was slow and prices declined, but strengthened at the close. New York Round Whites declined 25¢ to a close of $1.75 per 100 lbs. sacked f. o. b. shipping points and ranged 40¢ to 50¢ lower in Pittsburgh at $2 to $2.10. Bulk stock declined 25¢ to 50¢ in Philadelphia to a range of $1.75 to $2 the middle of the week, but recovered at the close and ruled $2.15, a net loss of 10¢ from last week’s price.

Northern Round Whites declined 70¢ in the Chicago carlot market, to a range of $1.65 to $1.85, but strengthened to a close of $1.90 to $2. In producing sections, prices declined 20¢ to 35¢ during the week, ranging $1.45 to $1.80, but closed stronger at $1.60 to $1.90 f. o. b. Idaho Rurals ruled 25¢ lower at $1.10 f. o. b. shipping points. Maine Irish Cobblers followed the general trend, showing a net loss at shipping points of 25¢ and closing at $1.11 to $1.21 per 100 lbs., bulk f. o. b. Green Mountains declined 10¢ to 20¢ and closed at $1.26 to $1.41. Cobblers declined 15¢ to 25¢ in consuming markets, bulk stock ranging $1.65 to $1.85 in New York and sacked stock $1.75 to $1.85 in Boston.

Sweet potatoes.—Sweet potato markets were well supplied, demand was slow to moderate and prices weakened. More than half the week’s supply in city markets was furnished by Virginia, now the leading shipping State. Yellow varieties from the Eastern Shore lost $1.25 in New York City, closing weak at $2.75 to $3 per bbl. This stock ranged $4 to $4.50 in Chicago and $4 to $4.25 in other markets. Tennessee Nancy Halls declined 10¢ to 30¢ in Chicago to a range of 90¢ to $1.15 per bushel hamper, but were firm in St. Louis at $1.15. New Jersey yellow varieties were about steady in New York at $1.50 to $1.60 per bushel hamper and in Pittsburgh at $2, but weakened slightly in Chicago to a range of $1.90 to $2.15.

Apples.—Apple markets were well supplied, demand was slow to moderate, and prices show some declines. New York Baldwins, A21⁄2, were steady at $6.50 to $7 per bbl. in New York, $7 to $7.50 in Philadelphia, and sold in Boston at $2.10 to $2.15 per bu. box. This stock closed 25¢ higher at $6.25 f. o. b. shipping points. New York Rhode Island Greenings declined 50¢, closing at $7.50 to $8.25 in Chicago, and at $8 to $9 in New York. Northwestern Extra Fancy Jonathans were firm early in the week in New York City at $4.75 to $5 per box, but declined to a close of $4 to $4.25. Total shipments of apples from all sections for the season were 17,288 cars, or slightly more than for last season to the same date. Boxed apple shipments were 3,568 cars, or nearly double last week’s movement and more than three times as heavy as for the same week a year ago. Washington with 1,864 cars exceeded last week’s entire boxed apple movement of 1,846 cars. Barreled apple shipments were 2,348 cars compared with 2,771 a year ago. New York, the heaviest shipping section, sent 1,301 cars.

Onions.—Demand for onions was slow and markets were dull in the East. Chicago held steady. Eastern yellow Globes No. 1 were firm in New York the middle of the week at $3.75 to $4 per 100 lbs. sacked, but declined later, reaching $3.25 to $3.50. Other markets were firm at $3.75 to $4. Middle western yellow stock strengthened in New York and Cincinnati, ranging $4 to $4.25, and declined 25¢ in Pittsburgh, clos- $3.75 to $4. California yellow and brown varieties were steady in Chicago at $4.25 to $4.50.

Cabbage.—Markets for cabbage were dull in producing sections, with slow demand and movement. New York Danish type stock declined $2, ranging $30 to $33 per ton bulk f. o. b.; domestic closed slightly higher than last week at $23 to $25. A decline of about $10 occurred in consuming markets. Domestic stock closed at $30 to $35 in New York and at $20 to $25 in Philadelphia. Northern Danish held steady in Chicago at $35 and at $40 in St. Louis. Cabbage shipments for the week were 682 cars, exceeding those for the same time last year, but showing a decrease from last week’s movement. New York shipped 197 cars, Wisconsin 177, and Colorado 154.

CARLOAD SHIPMENTS OF FRUITS AND VEGETABLES.

| Commodity. | Week of Sept. 25 to Oct. 1. |

September. | August. | July. | Season to Oct. 1. |

|||||

|---|---|---|---|---|---|---|---|---|---|---|

| 1921 | 1920 | 1921 | 1920 | 1921 | 1920 | 1921 | 1920 | 1921 | 1920 | |

| Apples: | ||||||||||

| Boxed | 3,568 | 1,109 | 6,188 | 2,048 | 1,005 | 846 | 368 | 278 | 8,277 | 3,440 |

| Barreled | 2,348 | 2,771 | 5,692 | 8,995 | 2,215 | 2,854 | 659 | 1,560 | 9,061 | 13,824 |

| Cabbage | 682 | 522 | 2,514 | 1,791 | 1,293 | 993 | 416 | 507 | 17,396 | 17,691 |

| Cantaloupes | 113 | 259 | 2,091 | 2,784 | 5,917 | 6,771 | 8,016 | 5,284 | 24,538 | 22,316 |

| Celery | 145 | 113 | 445 | 420 | 219 | 150 | 98 | 68 | 4,958 | 3,633 |

| Grapes | 4,316 | 3,466 | 15,496 | 12,001 | 2,810 | 4,647 | 363 | 366 | 19,332 | 17,652 |

| Lettuce | 300 | 132 | 1,280 | 832 | 1,113 | 934 | 1,377 | 980 | 16,453 | 11,847 |

| Onions | 730 | 932 | 3,074 | 3,674 | 1,816 | 1,899 | 1,403 | 1,031 | 11,758 | 13,344 |

| Peaches | 41 | 1,795 | 4,921 | 10,528 | 6,937 | 6,284 | 8,673 | 6,881 | 25,967 | 25,474 |

| Pears | 546 | 786 | 3,793 | 4,850 | 5,089 | 3,079 | 1,461 | 2,417 | 10,458 | 10,462 |

| Potatoes: | ||||||||||

| Sweet | 692 | 531 | 2,799 | 2,840 | 1,860 | 665 | 225 | 92 | 5,038 | 3,656 |

| White | 10,001 | 4,055 | 24,707 | 18,057 | 15,639 | 13,583 | 16,513 | 15,621 | 80,560 | 65,833 |

| Tomatoes | 387 | 692 | 2,468 | 3,434 | 995 | 1,604 | 1,644 | 2,180 | 15,074 | 13,652 |

| Watermelons | 91 | 92 | 1,788 | 2,174 | 11,435 | 10,299 | 19,206 | 20,199 | 44,172 | 39,109 |

| Vegetables (mixed) | 309 | 233 | 1,323 | 947 | 1,380 | 972 | 1,369 | 719 | 12,340 | 9,453 |

| Total | 24,269 | 17,488 | 78,579 | 75,375 | 59,723 | 55,580 | 61,791 | 58,183 | 305,382 | 271,386 |

PRICES OF FRUITS AND VEGETABLES.

Jobbing Range.

| POTATOES, Eastern and Northern Round-Whites, No. 1, per 100 lbs. sacked. |

||||||||||

| Market. | Car- loads re- ceived. |

This season. | One year ago. | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Oct. 3 | Sept. 26. | |||||||||

| New York | 428 | [1]$1.65 | - | $1.80 | [1]$2.20 | - | $2.30 | [2]$1.70 | - | $1.80 |

| Boston | 270 | [1]1.75 | - | 1.85 | [1]2.00 | [1]1.75 | - | 1.85 | ||

| Philadelphia | 202 | [1]2.00 | - | 2.15 | 2.25 | 2.00 | ||||

| Pittsburgh | 178 | 2.00 | - | 2.10 | 2.50 | 2.50 | - | 2.65 | ||

| Cincinnati | 69 | 2.35 | 2.50 | - | 2.65 | 2.35 | ||||

| Chicago | 701 | [3]1.90 | - | 2.00 | [3]2.35 | - | 2.50 | [3]2.00 | - | 2.25 |

| St. Louis | 99 | [4]2.25 | - | 2.30 | [4]2.50 | - | 2.65 | 2.30 | - | 2.40 |

| Kansas City | 217 | [4]2.00 | - | 2.10 | [4]2.30 | [4]1.75 | - | 2.00 | ||

| SWEET POTATOES, Virginia Eastern Shore Yellow Varieties, Barrels. |

||||||||||

| New York | 109 | $2.75 | - | $3.00 | $3.50 | - | $4.00 | $3.75 | - | $4.25 |

| Boston | 32 | 4.00 | - | 4.25 | 4.00 | - | 4.25 | 4.25 | - | 4.50 |

| Philadelphia | 1 | 4.00 | 3.25 | ... | ||||||

| Pittsburgh | 28 | 4.00 | - | 4.15 | 4.00 | 4.25 | - | 4.50 | ||

| Cincinnati | 11 | 4.00 | - | 4.25 | 4.25 | - | 4.50 | 4.00 | - | 4.25 |

| Chicago | 41 | 4.00 | - | 4.50 | 4.50 | - | 4.75 | 4.25 | - | 4.75 |

| St. Louis | 1 | [5]1.15 | [5]1.10 | - | 1.15 | [5]1.25 | ||||

| Kansas City | ... | [5]1.00 | - | 1.10 | [5]1.15 | - | 1.25 | ... | ||

| ONIONS, Eastern and Middle Western Yellow Globes, No. 1, per 100 lbs. sacked. |

||||||||||

| New York | 99 | $3.25 | - | $3.50 | $3.50 | - | $3.75 | $1.75 | - | $1.90 |

| Boston | 30 | 3.75 | 3.50 | - | 3.75 | 1.50 | - | 1.60 | ||

| Philadelphia | 30 | 4.00 | 3.25 | - | 4.00 | 1.25 | - | 1.60 | ||

| Pittsburgh | 40 | 3.75 | - | 4.00 | 3.75 | - | 4.25 | 1.50 | - | 1.75 |

| Cincinnati | 9 | 4.25 | 3.75 | - | 4.25 | 1.50 | ||||

| Chicago | 90 | 3.75 | - | 4.00 | 3.50 | - | 3.75 | 1.75 | - | 1.90 |

| St. Louis | 29 | [6]3.50 | - | 3.75 | [6]3.75 | [6]1.85 | - | 2.00 | ||

| Kansas City | 30 | [6]3.00 | - | 3.25 | [6]2.25 | [6]1.75 | ||||

| CABBAGE, New York and Northern Domestic, per Ton Bulk. |

||||||||||

| New York | 29 | $30 | - | $35 | $40 | ... | ||||

| Philadelphia | 26 | 15 | - | 20 | $30 | - | 35 | $10 | - | $13 |

| Pittsburgh | 12 | [7]2.00 | - | 2.25 | [7]2.00 | - | 2.25 | 20 | ||

| Cincinnati | 10 | 24 | - | 25 | 35 | - | 40 | 18 | - | 20 |

| Chicago | 38 | [8]35 | 24 | - | 25 | 8 | - | 9 | ||

| St. Louis | 57 | [8]40 | 35 | - | 40 | 30 | - | 35 | ||

| Kansas City | 48 | [7]1.75 | [7]2.25 | [7]1.50 | ||||||

| APPLES, New York and Maine Baldwins and Fall Varieties, A21⁄2, Barrels. |

||||||||||

| New York | 408 | $6.50 | - | $7.00 | $8.00 | - | $12.00 | $5.00 | - | $5.50 |

| Boston | 121 | 8.00 | - | 9.00 | 6.00 | - | 10.00 | 4.00 | ||

| Philadelphia | 118 | 7.00 | - | 7.50 | 8.00 | - | 10.50 | 4.50 | ||

| Pittsburgh | 92 | 8.00 | - | 8.50 | 7.00 | 4.00 | - | 4.50 | ||

| Cincinnati | 100 | 8.00 | - | 8.50 | 8.00 | - | 8.50 | ... | ||

| Chicago | 403 | 8.25 | - | 9.00 | 8.00 | - | 8.50 | 5.50 | - | 6.00 |

| Kansas City | 99 | ... | ... | [9]7.00 | - | 8.00 | ||||

| Prices f. o. b. Shipping Points. | ||||||||||

| POTATOES (100 lbs. sacked). |

||||||||||

| Rochester, N. Y. | $1.75 | $2.00 | ... | |||||||

| Presque Isle, Me. | [7]$1.26 | - | 1.41 | [7]1.46 | - | 1.52 | [7]$1.30 | - | $1.35 | |

| Grand Rapids, Mich. | 1.75 | - | 1.80 | 1.95 | - | 2.10 | 2.00 | |||

| Waupaca, Wis. | 1.60 | - | 1.90 | 1.95 | 1.80 | - | 1.85 | |||

| Minneapolis, Minn. | 1.65 | - | 1.85 | 1.70 | - | 1.95 | 1.75 | - | 1.90 | |

| Alliance, Nebr. | 1.80 | 1.70 | - | 1.95 | 1.50 | |||||

| Idaho Falls, Idaho | 1.10 | 1.35 | [10]1.10 | - | 1.15 | |||||

| Greeley, Colo. | [10]1.15 | - | 1.25 | [10]1.40 | [10]1.10 | - | 1.15 | |||

| CABBAGE (ton bulk). |

||||||||||

| Rochester, N. Y. | 30.00 | 32.00 | - | 35.00 | 10.00 | |||||

| ONIONS (100 lbs. sacked). |

||||||||||

| Massachusetts Points | 3.50 | 3.50 | - | 3.75 | 1.40 | - | 1.60 | |||

| APPLES. | ||||||||||

| Barreled: | ||||||||||

| Rochester, N. Y. | 6.25 | 6.00 | 3.50 | - | 4.00 | |||||

| Boxed: | ||||||||||

| Spokane, Wash. | 2.00 | - | 2.15 | 2.25 | 2.00 | - | 2.35 | |||

[1] Maine Irish Cobblers.

[2] Maine Irish Cobblers, bulk 100 lbs.

[3] Carlot sales.

[4] Minnesota Red River Ohios.

[5] Tennessee Nancy Halls.

[6] Red varieties.

[7] Bulk 100 lbs.

[8] Danish type.

[9] Missouri Jonathans.

[10] Wagonloads, cash to growers.

New York and Michigan Concord grapes in 12-qt. climax baskets declined 10¢ to 25¢ in New York and Boston, ranging 75¢ to $1.10, and closed lower in Chicago at $1 to $1.25. Niagaras were weak in New York at 75¢ to 85¢. New York cauliflower was slow and dull in Philadelphia at $1.75 per crate, and ranged $2 to $2.25 in other markets. Michigan Golden Heart celery in highball crates was slow and steady in Chicago and St. Louis at $1 to $1.25 and ranged $1.75 to $2 in Pittsburgh. Massachusetts cranberries were steady in Boston at $5 to $6 per 1⁄2-barrel crate, and at $6.25 to $6.50 in Pittsburgh and Cleveland. New York Bartlett pears ranged $3.25 to $3.50 per bushel basket in leading markets.

The potato crop in Aroostook Co., Me., promises to be the largest ever produced in northern Maine. Early plantings were damaged somewhat by dry weather, but the later plantings have developed fully, and the stock has become overgrown in many cases. The yield of Irish Cobblers will average 120 to 150 bbls. to the acre, with some yields as high as 200 bbls.

With a probable demand from a wide territory there is much local confidence in the outcome of the marketing season, especially after the first of the year. During the rise in the market the first week of September large quantities of potatoes were sold on a basis of $3 per bbl. to the grower, but many of these shipments were marketed at a loss. Large quantities of potatoes are being stored because of the generally low price level. Much of the stock that is being sold is that for which storage space can not be obtained or which must be sold for financial reasons. The growers generally feel that they should have $1.75 per 100 lbs. bulk.

The first heavy frost of the season came Sept. 21, and digging of all varieties will be pushed from now on. Shipments will continue moderately heavy and would undoubtedly become very heavy with stronger market conditions.

Top price of the season in New York was $1,150 per car. The general range in June in New York was $450 to $900 and in July $250 to $550. No sales of medium sizes were reported in Philadelphia above $900 and prevailing ranges during June were $400 to $700, but declines to a range of $250 to $500 occurred in July. Sales in Boston ranged nearly as high as in New York, allowing 1,000 melons per carload. Early quotations in Boston ranged 60¢ to $1.10 per melon, but price declined in July to a range of 30 to 65¢. Pittsburgh carlot sales ranged $500 to $1,025 in May and June and $250 to $500 in July. Chicago market quoted a top of $1,100 the last of May, but prevailing early ranges were $500 to $800 and July sales $200 to $600.

In the table “Carlot shipments of cantaloupes” on page 217 of the The Market Reporter for Oct. 1. the last column should be headed “To Sept. 17, 1920,” and the next to last column headed “To Sept. 17, 1921.”

Shipments of watermelons by the end of September somewhat exceeded 44,000 cars. The movement had surpassed that of last year by nearly 5,000 cars and was much larger than that of any preceding year.

The great Florida-Georgia-South Carolina melon section has shipped about 25,000 cars. Three other States, Texas, California, and Missouri, shipped 3,000 to 5,000 cars each; Alabama and North Carolina shipped over 1,000 each; Arkansas, Indiana, Oklahoma, 400 to 700 each; and 14 other States in smaller amounts. The season’s movement not only has exceeded the previous record-breaking volume of 1920 but is one-half greater than that of 1919 or of 1917 and more than double that of 1918.

Production the past three years has tended to increase rapidly in nearly all the leading watermelon States. Nearly 30,000 acres were planted in Texas compared with 38,000 in Georgia, the leading State, but shipments from Texas were greatly reduced by unfavorable weather. In most other sections conditions were favorable. Taking the watermelon section as a whole, there was a greater production from an acreage about the same as in 1920.

The East has been aggressively increasing its hold on the commercial production of watermelons during the past few seasons. Of the 5,000 cars constituting this season’s excess of shipments as compared with the movement last year, 3,000 cars came from the Southeast, about 1,000 cars from the Middle West, and a few hundred cars from the Far West.

The 1921 crop for the most part was of excellent grade. The size of Florida melons was reduced by drought, but conditions improved as the growing season moved northward.

The 1921 season opened with prices as high as in any preceding season. First sales in May exceeded $1,000 per car for medium sizes in New York, Chicago, and Pittsburgh. Similar prices were reported at the opening of the 1920 season and there were a few opening sales of medium size melons around $1,000 in 1919. In 1918 ranges in the early part of the season were only about one-half those of 1919 and were still lower in 1917 and 1916.

Prices in 1921 were not so well sustained as in 1920. During July heavy shipments from Georgia depressed the markets rapidly. July opened with carlot sales at $250 to $650 in city markets, but the range soon declined, reaching $200 to $250. The first week of August prices reached the low point of the season at $150 to $250 per car but recovered about $25 toward the end of the season of heavy shipments.

Prices opened at $300 to $515 f. o. b. Florida shipping points with top of $625, but declined rapidly with the beginning of the Georgia shipping season. Florida and Georgia Tom Watsons ranged $200 to $650 in July. Carolina melons at times ranged slightly lower than Georgia stock.

Prices of Missouri watermelons ranged $100 to $200 per car the first week of August, $125 to $250 the second week, and $120 to $200 the third week. Texas melons sold early in July at $2.50 to $3 per 100 lbs. but ranged mostly $1.25 to $1.75 in August. Further details of the price ranges of the principal lines of watermelons are given in the accompanying tables.

Carlot Shipments of Watermelons.

| To Sept. 24. |

Total season. |

|||||

|---|---|---|---|---|---|---|

| 1921 | 1920 | 1917 | 1918 | 1919 | 1920 | |

| Alabama | 1,398 | 1,160 | 1,634 | 806 | 708 | 1,160 |

| Arkansas | 520 | 314 | 449 | 93 | 268 | 314 |

| California | 3,455 | 3,106 | 1,137 | 1,689 | 3,300 | 3,272 |

| Delaware | 496 | 177 | 511 | 303 | 327 | 177 |

| Florida | 5,457 | 6,807 | 3,622 | 2,179 | 3,878 | 6,807 |

| Georgia | 15,791 | 11,103 | 9,530 | 6,782 | 8,984 | 11,103 |

| Illinois | 309 | 247 | 386 | 68 | 190 | 251 |

| Indiana | 706 | 647 | 630 | 191 | 581 | 661 |

| Iowa | 681 | 330 | 238 | 132 | 321 | 348 |

| Maryland | 759 | 458 | 1,019 | 388 | 515 | 458 |

| Missouri | 3,089 | 3,008 | 2,533 | 1,196 | 3,516 | 3,012 |

| North Carolina | 1,219 | 799 | 1,201 | 727 | 891 | 799 |

| Oklahoma | 549 | 464 | 505 | 189 | 870 | 465 |

| South Carolina | 4,407 | 4,735 | 4,107 | 2,787 | 2,673 | 4,735 |

| Texas | 4,056 | 4,839 | 2,871 | 2,290 | 3,007 | 4,845 |

| Virginia | 338 | 312 | 728 | 244 | 263 | 312 |

| Other States | 851 | 506 | 402 | 328 | 568 | 530 |

| Total | 44,081 | 39,012 | 31,503 | 20,392 | 30,860 | 39,249 |

RANGES OF WATERMELON PRICES

F. O. B. Shipping Points.

[Bulk per car.]

| State and year. |

Weights quoted. |

Opening. | High. | Low. | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Week ending— |

Price. | Week ending— |

Price. | Week ending— |

Price. | |||||||||||||

| Florida: | Pounds. | |||||||||||||||||

| 1921 | 22 | - | 28 | May | 23 | $350 | - | $600 | May | 23 | $350 | - | $600 | July | 11 | $200 | - | $250 |

| 1920 | 22 | - | 28 | June | 14 | 250 | - | 500 | June | 14 | 250 | - | 500 | June | 28 | 175 | - | 500 |

| 1919 | 22 | - | 28 | June | 9 | 400 | - | 550 | June | 9 | 400 | - | 550 | June | 23 | 300 | - | 475 |

| 1918 | 20 | - | 25 | June | 3 | 300 | - | 400 | June | 24 | 350 | - | 450 | June | 10 | 275 | - | 400 |

| 1917 | 20 | - | 25 | June | 11 | 140 | - | 200 | June | 18 | 165 | - | 225 | June | 11 | 140 | - | 200 |

| Georgia: | ||||||||||||||||||

| 1921 | 22 | - | 28 | June | 27 | 200 | - | 525 | June | 27 | 200 | - | 525 | Aug. | 8 | 40 | - | 125 |

| 1920 | 22 | - | 28 | July | 5 | 200 | - | 450 | July | 5 | 200 | - | 450 | July | 19 | 75 | - | 200 |

| 1919 | 22 | - | 27 | June | 30 | 250 | - | 450 | June | 30 | 250 | - | 450 | July | 28 | 125 | - | 250 |

| 1918 | 28 | - | 30 | July | 1 | 135 | - | 175 | July | 8 | 200 | - | 220 | July | 15 | 75 | - | 150 |

| 1917 | 20 | - | 25 | June | 25 | 175 | - | 265 | July | 2 | 175 | - | 275 | Aug. | 20 | 70 | - | 75 |

| Texas: | ||||||||||||||||||

| 1921 | 22 | - | 28 | July | 18 | 80 | - | 250 | July | 18 | 80 | - | 250 | Aug. | 1 | [1]25 | - | 50¢ |

| 1920 | 22 | - | 28 | July | 5 | 250 | - | 375 | July | 12 | 150 | - | 375 | July | 19 | 65 | - | 250 |

| 1919 | 22 | - | 28 | July | 21 | 250 | - | 400 | July | 21 | 250 | - | 400 | July | 28 | 150 | - | 300 |

| 1918 | 20 | - | 27 | June | 24 | 335 | - | 400 | June | 24 | 335 | - | 400 | July | 22 | 100 | - | 200 |

| 1917 | 20 | - | 25 | July | 2 | 200 | - | 290 | July | 2 | 200 | - | 290 | July | 16 | 100 | - | 200 |

| Missouri: | ||||||||||||||||||

| 1921 | 22 | - | 28 | Aug. | 1 | 165 | - | 340 | Aug. | 1 | 165 | - | 340 | Aug. | 22 | 65 | - | 150 |

| 1920 | 22 | - | 28 | Aug. | 2 | 200 | - | 325 | Aug. | 9 | 300 | - | 425 | Aug. | 16 | 200 | - | 350 |

| 1919 | 22 | - | 28 | Aug. | 4 | 250 | - | 450 | Aug. | 4 | 250 | - | 450 | Aug. | 11 | 125 | - | 300 |

| 1918 | 20 | - | 25 | Aug. | 5 | 230 | - | 300 | Aug. | 12 | 300 | - | 400 | Aug. | 5 | 230 | - | 300 |

| 1916 | 22 | - | 27 | Aug. | 7 | 135 | - | 200 | Aug. | 14 | 110 | - | 175 | Aug. | 21 | 65 | - | 165 |

[1] Bulk per 100 lbs.

Sales to Jobbers in Leading Consuming Markets.

| State and variety. |

Year. | Weights quoted. |

Opening. | High. | Low. | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Week ending— |

Price. | Week ending— |

Price. | Week ending— |

Price. | ||||||||||||||

| Pounds. | |||||||||||||||||||

| Florida, Tom Watsons | 1921 | 22 | - | 28 | May | 23 | $1,150 | May | 30 | $600 | - | 1,200 | July | 25 | 250 | - | 450 | ||

| 1920 | 22 | - | 28 | June | 14 | 500 | - | 1,100 | June | 14 | 500 | - | 1,100 | July | 12 | 300 | - | 500 | |

| 1919 | 23 | - | 28 | June | 9 | 750 | - | 1,050 | June | 9 | 750 | - | 1,050 | July | 14 | 300 | - | 550 | |

| 1918 | 20 | - | 25 | June | 3 | 300 | - | 500 | June | 24 | 550 | - | 800 | July | 8 | 300 | |||

| 1917 | 20 | - | 25 | June | 11 | 250 | - | 350 | July | 2 | 300 | - | 450 | July | 10 | 150 | - | 225 | |